Exploring the best saving schemes in post office? You are in the right place. India Post offers some of the safest, highest yielding, and most trusted small savings schemes available to Indian citizens. Backed by the Government of India, these schemes have helped crores of families build wealth, save taxes, and achieve their financial goals for decades.

Whether you are saving for your child’s future, planning your retirement, building an emergency fund, or simply looking for a safe place to park your money with assured returns, the post office has a scheme designed for every life stage and goal. With interest rates ranging from 4 percent on savings accounts to 8.2 percent on flagship schemes like SCSS and SSY, these government backed instruments often outperform regular bank fixed deposits.

In this complete guide, you will discover all the major post office savings schemes available in India, their latest interest rates, eligibility criteria, tax benefits, lock in periods, and how to open accounts. Let us dive in.

Why Choose Post Office Savings Schemes?

Before exploring the schemes, here is why post office savings schemes have remained popular for generations.

Government backing. Every post office scheme is fully backed by the Government of India, making them virtually risk free with sovereign guarantee.

Higher interest rates. Most post office schemes offer interest rates that are higher than bank savings accounts and often competitive with bank FDs.

Wide accessibility. With over 1.5 lakh post offices across India, including thousands in rural areas, post office schemes are accessible to almost every Indian.

Tax benefits. Many schemes qualify for deduction under Section 80C, and some offer fully tax free returns.

Diverse options. From short term to long term, monthly income to lump sum maturity, there is a scheme for every need.

No hidden fees. Unlike many private financial products, post office schemes have transparent, simple structures without hidden charges.

According to the Department of Posts (India Post), small savings schemes administered through post offices continue to be one of the most preferred savings options for Indian households due to their safety, attractive interest rates, and ease of access.

All Saving Schemes in Post Office: Complete List With Interest Rates

Here is the complete breakdown of every major post office saving scheme available in India with current interest rates.

1. Post Office Savings Account (POSA)

The Post Office Savings Account works similar to a regular bank savings account but is operated through post offices.

Interest rate: 4 percent per annum

Key features:

- Minimum deposit of 500 rupees to open and maintain the account

- Cheque book, ATM card, mobile banking, and e banking facilities available

- Interest credited annually

- Tax benefit under Section 80TTA up to 10,000 rupees of interest per year (50,000 for senior citizens under 80TTB)

Best for: Safe day to day savings with full liquidity. Compare it with our complete guide on the best bank for savings account in India to choose between them.

2. Post Office Recurring Deposit (RD)

The 5 Year Post Office RD is a popular monthly savings scheme that helps you build a corpus gradually.

Interest rate: 6.7 percent per annum (compounded quarterly)

Key features:

- Minimum deposit of 100 rupees per month (then in multiples of 10)

- No maximum limit

- Fixed tenure of 5 years

- Loan facility available against deposits after 1 year

- Premature closure allowed after 3 years

Best for: Beginners building monthly savings habits with guaranteed returns.

3. Post Office Time Deposit (TD or POTD)

Post Office Time Deposits work like bank fixed deposits, offering you fixed returns for chosen tenures.

Interest rates:

- 1 year time deposit: 6.9 percent per annum

- 2 year time deposit: 7.0 percent per annum

- 3 year time deposit: 7.1 percent per annum

- 5 year time deposit: 7.5 percent per annum

Key features:

- Minimum deposit of 1,000 rupees, then in multiples of 100

- No maximum limit

- 5 year TD qualifies for Section 80C tax deduction

- TDS not applicable (unlike bank FDs)

- Premature withdrawal allowed after 6 months with reduced interest

Best for: Investors seeking safe, fixed returns with government backing.

For more FD comparisons, also check our guide on banks that give higher interest rate in India.

4. Post Office Monthly Income Scheme (POMIS)

POMIS is one of the most popular schemes for those seeking regular monthly income.

Interest rate: 7.4 percent per annum (paid monthly)

Key features:

- Minimum deposit of 1,000 rupees

- Maximum 9 lakh rupees in single account

- Maximum 15 lakh rupees in joint account

- 5 year tenure

- Monthly interest credited to your savings account

- Premature closure allowed after 1 year with penalty

- No TDS

Best for: Retirees and individuals needing steady monthly cash flow.

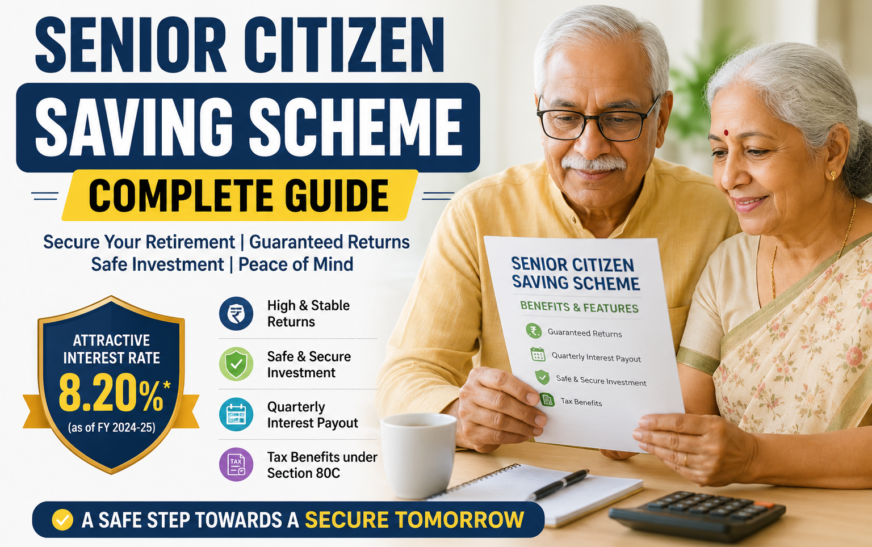

5. Senior Citizen Saving Scheme (SCSS)

SCSS is one of the highest paying post office schemes designed exclusively for senior citizens.

Interest rate: 8.2 percent per annum (paid quarterly)

Key features:

- Available for individuals aged 60 and above

- Early retirees aged 55 to 60 eligible under specific conditions

- Minimum deposit of 1,000 rupees, maximum 30 lakh rupees

- Tenure of 5 years (extendable by 3 years)

- Section 80C tax deduction available

- Interest paid quarterly

Best for: Senior citizens seeking safe high yielding retirement income.

Learn more in our complete Senior Citizen Saving Scheme guide with detailed examples and tips.

6. Public Provident Fund (PPF)

PPF is one of India’s most loved long term investment schemes thanks to its triple tax benefit (EEE status), meaning tax free deposits, tax free interest, and tax free maturity.

Interest rate: 7.1 percent per annum (compounded annually)

Key features:

- Minimum deposit of 500 rupees per year, maximum 1.5 lakh rupees per year

- Tenure of 15 years (extendable in 5 year blocks)

- Section 80C tax deduction up to 1.5 lakh rupees

- Completely tax free returns (EEE status)

- Loan facility available between years 3 to 6

- Partial withdrawal allowed from year 7

Best for: Long term, tax free wealth building and retirement planning. PPF is one of the strongest investment options for beginners in India.

7. Sukanya Samriddhi Yojana (SSY)

SSY is a special savings scheme designed for the financial future of a girl child in India.

Interest rate: 8.2 percent per annum (compounded annually)

Key features:

- Available only for girl children below 10 years of age

- Minimum deposit of 250 rupees per year, maximum 1.5 lakh rupees per year

- Account matures when the girl turns 21 (or after marriage post age 18)

- Section 80C tax deduction

- Completely tax free returns (EEE status)

- Account can be opened in the name of up to 2 girl children per family (3 in case of twins/triplets)

Best for: Parents saving for their daughter’s education and marriage.

8. National Savings Certificate (NSC)

NSC is a popular 5 year savings certificate offering guaranteed returns and tax benefits.

Interest rate: 7.7 percent per annum (compounded annually but paid at maturity)

Key features:

- Minimum deposit of 1,000 rupees, no maximum limit

- 5 year lock in period

- Section 80C tax deduction

- Interest accrued each year is reinvested and qualifies for 80C deduction (except final year)

- Can be used as collateral for loans

- Available in denominations of 1,000, 5,000, 10,000, and so on

Best for: Tax saving with assured returns and short to medium term goals.

9. Kisan Vikas Patra (KVP)

Kisan Vikas Patra is a savings certificate that doubles your money over a fixed period.

Interest rate: 7.5 percent per annum (currently maturity at around 115 months)

Key features:

- Minimum deposit of 1,000 rupees, no maximum limit

- Doubles the invested amount in about 115 months (approximately 9 years 7 months)

- Available in denominations of 1,000, 5,000, 10,000, and 50,000

- Can be transferred from one person to another

- No tax benefits under Section 80C

- TDS applicable on interest

Best for: Investors looking for guaranteed doubling of money over the long term.

10. Mahila Samman Savings Certificate (MSSC)

The Mahila Samman Savings Certificate is a special scheme launched by the Government of India for women.

Interest rate: 7.5 percent per annum (compounded quarterly)

Key features:

- Available exclusively for women and girl children

- Minimum deposit of 1,000 rupees, maximum 2 lakh rupees

- Fixed tenure of 2 years

- Partial withdrawal allowed (up to 40 percent of balance after 1 year)

- TDS applicable on interest

- Can be opened in the name of any Indian woman or by a guardian for a girl child

Best for: Women seeking short term high return savings.

Post Office Savings Schemes Interest Rates at a Glance

Here is a quick summary of current post office scheme interest rates for easy comparison.

Highest paying schemes:

- Senior Citizen Saving Scheme (SCSS): 8.2 percent per annum

- Sukanya Samriddhi Yojana (SSY): 8.2 percent per annum

Medium yield schemes:

- National Savings Certificate (NSC): 7.7 percent per annum

- 5 Year Post Office Time Deposit: 7.5 percent per annum

- Mahila Samman Savings Certificate: 7.5 percent per annum

- Post Office MIS: 7.4 percent per annum

- Kisan Vikas Patra (KVP): 7.5 percent per annum

- PPF: 7.1 percent per annum

- 3 Year Post Office TD: 7.1 percent per annum

Lower yield schemes:

- 2 Year Post Office TD: 7.0 percent per annum

- 1 Year Post Office TD: 6.9 percent per annum

- 5 Year Post Office RD: 6.7 percent per annum

- Post Office Savings Account: 4.0 percent per annum

Important: All small savings scheme interest rates are reviewed and revised quarterly by the Ministry of Finance, Government of India.

Tax Benefits of Post Office Saving Schemes

Many post office schemes offer significant tax benefits under various sections of the Income Tax Act.

Section 80C Eligible Schemes (Up to 1.5 Lakh Rupees Deduction)

- Public Provident Fund (PPF)

- Sukanya Samriddhi Yojana (SSY)

- Senior Citizen Saving Scheme (SCSS)

- 5 Year Post Office Time Deposit

- National Savings Certificate (NSC)

Tax Free Returns (EEE Status)

- Public Provident Fund (PPF)

- Sukanya Samriddhi Yojana (SSY)

Taxable Interest (As Per Income Slab)

- Post Office Savings Account (above 10,000 rupees of interest)

- Post Office RD

- Post Office Time Deposits (1, 2, 3 year)

- Post Office MIS

- KVP

- SCSS (above 1 lakh rupees of interest for seniors)

- Mahila Samman Savings Certificate

Important note: Section 80C benefits are only available under the old tax regime. Under the new tax regime (default since 2023), 80C deductions are not available. Visit the Income Tax Department of India website for full details.

How to Open a Post Office Savings Account

Opening a post office savings account is simple. Here is the step by step process.

Step 1: Visit your nearest post office or download the application form from the India Post website.

Step 2: Fill out the account opening form for the scheme you wish to open.

Step 3: Submit the required documents:

- Identity proof (Aadhaar, PAN, Voter ID, or passport)

- Address proof (Aadhaar, utility bill, or rental agreement)

- Two passport size photographs

- Age proof (if required)

- KYC documents

- PAN card (mandatory for most schemes)

Step 4: Make the initial deposit through cash, cheque, or demand draft.

Step 5: Collect your passbook and any certificates.

You can also open many post office schemes online through India Post’s POSB digital banking platform or via Aadhaar based e KYC at participating banks.

How to Choose the Right Post Office Scheme

With multiple options available, picking the right scheme depends on your financial goals. Use this simple framework.

Short term goals (1 to 3 years):

- Post Office Time Deposits (1, 2, or 3 year)

- Mahila Samman Savings Certificate (2 years, women only)

- Recurring Deposit

Medium term goals (3 to 5 years):

- 5 Year Post Office TD

- NSC

- Post Office RD

- POMIS for monthly income

Long term goals (10+ years):

- PPF for tax free wealth building

- Sukanya Samriddhi Yojana (for girl child)

- KVP for doubling money

Retirement and senior income:

- Senior Citizen Saving Scheme

- POMIS for monthly income

- 5 Year TD

Tax saving:

- PPF

- SSY

- NSC

- 5 Year TD

- SCSS

For long term financial planning, pair these schemes with our complete guide on 15 personal finance tips.

Tips to Maximize Returns from Post Office Schemes

Use these proven strategies to get the most out of your post office investments.

Start early with PPF. Even small monthly contributions to PPF starting in your 20s can grow into 1 crore rupees by retirement, completely tax free.

Combine schemes for maximum benefit. Use PPF for long term wealth, SCSS for senior income, SSY for daughters, NSC for tax saving, and TDs for short term goals.

Reinvest interest from RD and MIS. Use monthly POMIS interest to fund SIPs in mutual funds or top up your PPF for accelerated growth.

Use the higher SCSS limit. A senior couple can together invest up to 60 lakh rupees in SCSS (30 lakh rupees each) for nearly 41,000 rupees monthly income.

Submit Form 15H or 15G. If your total income is below the taxable limit, submit Form 15H (seniors) or Form 15G (others) at the start of each financial year to avoid TDS deduction.

Open scheme in spouse’s name. Where applicable, having accounts in both spouses’ names doubles tax benefits and investment limits.

Use IPPB for digital convenience. India Post Payments Bank (IPPB) lets you operate many post office schemes digitally without visiting a branch.

Track all your investments. Use one of the best apps for managing personal money in India to keep track of multiple post office schemes in one place.

Common Mistakes to Avoid With Post Office Schemes

Avoid these traps that cost most investors over time.

Ignoring quarterly rate revisions. Open accounts when rates are at their peak. Once opened, the rate is usually locked or follows quarterly changes for the duration.

Not nominating beneficiaries. Always nominate to avoid legal complications later. Most schemes allow up to 4 nominees.

Withdrawing prematurely without need. Penalties on early withdrawal can wipe out months of returns. Plan your liquidity properly.

Forgetting to invest in PPF every year. Missing yearly minimum 500 rupees deposit in PPF makes the account inactive. Pay 50 rupees penalty plus the missed deposit to revive it.

Ignoring SSY for daughters. Many parents miss this incredible 8.2 percent EEE scheme for girl children. Open it before your daughter turns 10.

Maxing 80C in just one scheme. Diversify your 1.5 lakh rupees 80C investment across PPF, ELSS, and life insurance for better balance.

Not extending PPF. After 15 years, PPF can be extended in 5 year blocks indefinitely. Keep extending if you do not need the corpus immediately.

Post Office Schemes vs Bank Fixed Deposits

Post office schemes and bank FDs are two of the most popular safe investments in India. Here is a quick comparison.

Post office schemes advantages:

- Government backed, sovereign guarantee (safer than DICGC’s 5 lakh rupees limit)

- Higher interest rates on most schemes

- No TDS on time deposits (unlike bank FDs)

- Wider accessibility through 1.5 lakh+ post offices

Bank FD advantages:

- More flexible tenures (7 days to 10 years)

- Easier online opening and management

- Often easier premature withdrawal

- Higher rates in small finance banks (up to 8 to 8.5 percent)

The smart approach is to use both. Keep a portion in post office schemes for safety and tax benefits, and diversify with bank FDs for liquidity and higher rates on specific tenures.

Frequently Asked Questions (FAQs)

What are the saving schemes in post office?

The post office in India offers 10 main saving schemes including Post Office Savings Account (POSA), Recurring Deposit (RD), Time Deposit (TD), Monthly Income Scheme (MIS), Senior Citizen Saving Scheme (SCSS), Public Provident Fund (PPF), Sukanya Samriddhi Yojana (SSY), National Savings Certificate (NSC), Kisan Vikas Patra (KVP), and Mahila Samman Savings Certificate (MSSC).

Which post office scheme has the highest interest rate?

The Senior Citizen Saving Scheme (SCSS) and Sukanya Samriddhi Yojana (SSY) currently offer the highest interest rates at 8.2 percent per annum among post office schemes. SCSS is for senior citizens above 60, while SSY is for girl children below 10 years.

Is investment in post office schemes safe?

Yes, post office schemes are among the safest investments in India because they are fully backed by the Government of India with sovereign guarantee. There is virtually zero capital risk compared to market linked instruments.

Are post office scheme returns tax free?

Some post office schemes offer tax free returns, including PPF and Sukanya Samriddhi Yojana (EEE status). Others like SCSS, MIS, NSC, KVP, and TDs offer taxable returns. PPF and SSY also qualify for Section 80C tax deduction up to 1.5 lakh rupees.

What is the minimum amount to invest in post office schemes?

The minimum amounts vary by scheme. Post Office Savings Account requires just 500 rupees, RD starts at 100 rupees per month, PPF needs 500 rupees per year, SSY starts at 250 rupees per year, and most other schemes start at 1,000 rupees.

Can NRIs invest in post office schemes?

No, Non Resident Indians (NRIs) cannot invest in most post office savings schemes. If a resident becomes an NRI during the scheme’s tenure, the account is treated under specific rules. Hindu Undivided Families (HUFs) also cannot invest in most post office schemes.

Is TDS applicable on post office scheme interest?

TDS is not applicable on Post Office Time Deposits or Recurring Deposits (unlike bank FDs). However, TDS applies to MIS, KVP, NSC, SCSS (above 1 lakh rupees), and Mahila Samman Savings Certificate if interest crosses certain thresholds. PPF and SSY are completely tax free.

Can I open multiple post office accounts?

Yes, you can open multiple accounts across different schemes. However, certain schemes have limits. For example, PPF allows only one account per person, and SCSS deposits across all accounts cannot exceed 30 lakh rupees.

How is interest calculated in post office schemes?

Interest calculation varies by scheme. PPF interest is compounded annually, RD and POSA interest is compounded quarterly, SCSS interest is paid quarterly, MIS pays monthly, and NSC accrues annually with maturity payout. Always check the specific scheme rules.

How do I open a post office account online?

You can open many post office accounts online through India Post’s POSB digital banking platform or through India Post Payments Bank (IPPB) using Aadhaar based e KYC. For full online opening, you need PAN, Aadhaar, and an Aadhaar linked mobile number. Some schemes still require physical verification at your local post office.

Final Thoughts

Investing in saving schemes in post office is one of the smartest financial moves any Indian can make for guaranteed safety, attractive returns, and significant tax benefits. With more than 10 well designed schemes covering every life goal, from short term savings to retirement planning, the post office continues to be the backbone of safe investing in India.

The smart strategy is to combine multiple post office schemes to match your different goals. Use PPF and SSY for long term tax free wealth building, SCSS for senior retirement income, POMIS for steady monthly cash flow, NSC for tax saving, and post office TDs for short term goals. Pair these with smart equity investments and an emergency fund in a high interest savings account to build a complete financial plan.

Remember, the interest rates on these schemes are reviewed every quarter. Always check the latest rates before opening a new account, and consider locking in attractive rates with longer tenure schemes whenever possible.

To take your money journey even further, also explore our complete guides on investment options for beginners in India, banks that give higher interest rate in India, and passive income ideas that actually work to build long term wealth.

Which post office saving scheme will you start with first? Visit your nearest post office today, take the first step, and share your experience in the comments below.

Disclaimer: Interest rates, eligibility criteria, and scheme features mentioned in this article are based on the most recent publicly available data at the time of writing and may change without notice. All small savings scheme rates are revised quarterly by the Ministry of Finance. Always verify the latest details directly from the India Post website or the RBI website before investing. This article is for informational purposes only and does not constitute financial advice. Always consult a SEBI registered financial advisor before making investment decisions.