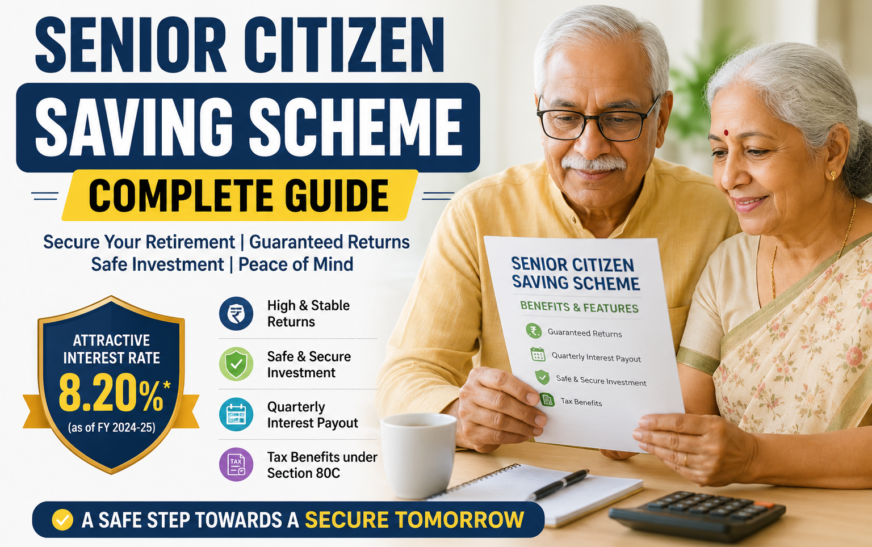

Looking for complete details on the Senior Citizen Saving Scheme (SCSS)? You are in the right place. SCSS is one of the safest, highest yielding, and most popular government backed investment options in India, designed exclusively for senior citizens aged 60 years and above. With guaranteed returns, quarterly interest payouts, tax benefits, and full government backing, it has become a go to choice for millions of retirees seeking steady post retirement income.

Whether you are planning your own retirement, helping your parents invest their retirement corpus, or simply researching the safest investment options for seniors in India, the SCSS deserves serious consideration. The scheme currently offers one of the highest interest rates among small savings schemes in India and helps protect your principal while delivering predictable quarterly income for living expenses.

In this complete guide, you will discover everything you need to know about the Senior Citizen Saving Scheme, including the latest interest rate, eligibility, benefits, tax rules, how to open an account, and how to maximize your returns. Let us dive in.

What Is the Senior Citizen Saving Scheme (SCSS)?

The Senior Citizen Saving Scheme is a government backed retirement savings program launched in 2004 under the post office small savings umbrella. It is designed to provide financial security and a steady regular income to Indian citizens aged 60 years and above.

The scheme is operated through authorized public and private banks as well as post offices across India. You can open the account individually or jointly with your spouse. Since it is fully backed by the Government of India, your money is completely safe, and the returns are guaranteed.

According to the Department of Posts (India Post), the SCSS continues to be one of the most preferred savings schemes for senior citizens due to its safety, attractive interest rates, and ease of access.

SCSS Interest Rate

The Senior Citizen Saving Scheme currently offers an interest rate of 8.2 percent per annum, making it one of the highest paying fixed income small savings schemes in India.

Key points about SCSS interest:

- The interest rate is reviewed and notified quarterly by the Government of India

- Interest is calculated and credited quarterly to your SCSS account

- Once you open the account at a given rate, that rate is locked in for the full 5 year tenure

- Interest is paid on the 1st of April, July, October, and January every year

- The current rate of 8.2 percent has been stable since April 2023

This higher than usual interest rate makes SCSS more attractive than most bank fixed deposits, especially for retirees seeking dependable income.

If you want to compare SCSS with other investment options, check out our complete guide on banks that give higher interest rate in India for FD comparisons.

Key Features of Senior Citizen Saving Scheme

The SCSS comes with several attractive features that make it a top choice for senior investors.

1. Government Backing

SCSS is fully backed by the Government of India, making it one of the safest investment options available. Your principal and interest are guaranteed by the sovereign, with zero capital risk.

2. High Interest Rate

The current SCSS interest rate of 8.2 percent per annum is significantly higher than most bank FDs and savings accounts, making it ideal for senior investors looking for safe high returns.

3. Tenure of 5 Years

The standard tenure of SCSS is 5 years from the date of account opening. After maturity, you can extend the account by an additional 3 years if you wish to continue earning.

4. Quarterly Interest Payouts

The interest earned on your SCSS deposit is paid every quarter, providing a regular and predictable income stream for daily expenses.

5. Investment Limits

You can invest a minimum of 1,000 rupees and a maximum of 30 lakh rupees across all your SCSS accounts combined. The maximum limit was previously 15 lakh rupees but was raised to 30 lakh rupees in the 2023 budget.

6. Multiple Account Options

You can open SCSS account individually or jointly with your spouse. However, the total deposits across all accounts cannot exceed the 30 lakh rupees limit.

7. Easy Premature Withdrawal

While SCSS has a 5 year lock in, you can make a premature withdrawal after one year with applicable penalties. This adds emergency liquidity if needed.

8. Tax Benefits

The principal amount invested in SCSS qualifies for tax deduction under Section 80C of the Income Tax Act, up to a maximum of 1.5 lakh rupees per financial year.

For more tax saving strategies, also check our complete guide on 15 personal finance tips.

SCSS Eligibility Criteria

Not everyone can open an SCSS account. Here are the detailed eligibility criteria.

Eligible to open SCSS account:

- Senior citizens: Any Indian citizen aged 60 years or above

- Early retirees: Civilian employees aged 55 to 60 years who have retired under superannuation or VRS can open an account within 1 month of receiving retirement benefits

- Defence personnel: Retired defence employees aged 50 to 60 years can open an account within 1 month of receiving retirement benefits

Not eligible:

- Non Resident Indians (NRIs)

- Hindu Undivided Families (HUFs)

- Persons of Indian Origin (PIOs)

You can hold the SCSS account individually or jointly only with your spouse. PAN and Aadhaar card are mandatory.

How to Open an SCSS Account

You can open a Senior Citizen Saving Scheme account at any post office or authorized bank branch. Here is the step by step process.

Step 1: Choose Where to Open the Account

You can open the SCSS account at any of these:

- India Post offices: Available across India. Visit your nearest post office or the India Post website for details.

- Authorized public and private banks including:

Step 2: Collect the SCSS Application Form

You can download the SCSS application form from the India Post website or get it directly from the post office or bank branch.

Step 3: Fill in the Application Form

Provide the following details:

- Full name as per PAN and Aadhaar

- Date of birth

- Address and contact details

- Deposit amount

- Nominee details (mandatory, you can nominate up to 4 people)

- Bank account details for interest credit

- Joint holder details (if applicable)

Step 4: Submit Required Documents

The standard documents required to open an SCSS account include:

- Identity proof: PAN card, Voter ID, Aadhaar card, or passport

- Address proof: Aadhaar card, telephone bill, electricity bill, or utility bill

- Age proof: PAN card, Voter ID, birth certificate, or senior citizen card

- Two passport size photographs

- Retirement proof (only for early retirees)

- Aadhaar card (mandatory)

- PAN card (mandatory)

All documents must be self attested.

Step 5: Make the Deposit

You can deposit the amount via cash (up to 1 lakh rupees only) or by cheque/demand draft for higher amounts. The deposit date is considered the date when the cheque or DD is realized.

Step 6: Receive the Passbook

After successful account opening, you will receive a passbook with all your account details. Keep it safe for future reference and withdrawals.

SCSS Tax Benefits

The Senior Citizen Saving Scheme offers attractive tax benefits that make it even more rewarding.

Section 80C Deduction

The principal amount invested in SCSS qualifies for tax deduction under Section 80C of the Income Tax Act, up to a maximum of 1.5 lakh rupees per year.

Important note: This benefit is only available under the old tax regime. Under the new tax regime (default since 2023), Section 80C benefits are not available.

Tax on SCSS Interest

While the principal qualifies for 80C deduction, the interest earned is fully taxable as per your income tax slab.

TDS (Tax Deducted at Source)

If the total interest income from SCSS exceeds 50,000 rupees in a financial year, TDS is deducted at 10 percent. However, starting from FY 2025–26, the TDS threshold has been increased to 1 lakh rupees for senior citizens, providing significant relief.

How to Avoid TDS

If your total income is below the taxable limit, you can submit Form 15H to your bank or post office at the start of each financial year. This declaration prevents TDS deduction at source.

For full tax planning details, visit the Income Tax Department of India website.

SCSS Calculator: How to Calculate Your Returns

Here is how you can calculate the returns from your SCSS investment.

Formula:

Quarterly Interest = (Investment Amount x Annual Interest Rate) / 4

Example calculations at 8.2 percent per annum:

For 1 lakh rupees invested:

- Quarterly interest: 2,050 rupees

- Annual interest: 8,200 rupees

- Total interest over 5 years: 41,000 rupees

- Total amount at maturity: 1,41,000 rupees

For 5 lakh rupees invested:

- Quarterly interest: 10,250 rupees

- Annual interest: 41,000 rupees

- Total interest over 5 years: 2,05,000 rupees

- Total amount at maturity: 7,05,000 rupees

For 15 lakh rupees invested:

- Quarterly interest: 30,750 rupees

- Annual interest: 1,23,000 rupees

- Total interest over 5 years: 6,15,000 rupees

- Total amount at maturity: 21,15,000 rupees

For 30 lakh rupees invested (maximum):

- Quarterly interest: 61,500 rupees

- Annual interest: 2,46,000 rupees

- Total interest over 5 years: 12,30,000 rupees

- Total amount at maturity: 42,30,000 rupees

You can use free SCSS calculators on Groww, ClearTax, or Paisabazaar for instant calculations.

SCSS vs Fixed Deposits: Which Is Better?

This is one of the most common questions for senior investors. Here is the honest comparison.

SCSS advantages:

- Higher interest rate (8.2 percent vs 6.5 to 8 percent for most bank FDs)

- Government backed safety (better than DICGC’s 5 lakh rupees insurance limit per bank)

- Section 80C tax benefit on principal

- Higher deposit limit (30 lakh rupees in one place)

Fixed Deposit advantages:

- More flexible tenure (7 days to 10 years)

- Available to non senior citizens too

- Can be opened entirely online

- Easier premature withdrawal

Verdict: For senior citizens looking for safe, high yielding investments, SCSS is generally better than bank FDs for the first 30 lakh rupees. After that, you can park additional amounts in high yielding bank FDs from top banks or small finance banks.

For more details on the best FD options, check our complete guide on banks that give higher interest rate in India.

SCSS Premature Withdrawal Rules

While SCSS has a 5 year lock in, you can withdraw early if needed. Here are the rules.

Premature withdrawal penalties:

- Withdrawal before 1 year: Not allowed

- Withdrawal between 1 to 2 years: 1.5 percent of the deposit amount is deducted

- Withdrawal between 2 to 5 years: 1 percent of the deposit amount is deducted

- Death of account holder: No penalty. Full amount is paid to nominee/legal heirs with applicable interest.

SCSS Account Extension After Maturity

After the initial 5 year tenure, you can extend your SCSS account by an additional 3 years. Here is how.

Key extension rules:

- The extension request must be made within 1 year of maturity

- The extended account will earn interest at the rate applicable on the date of maturity

- You can prematurely withdraw the extended account anytime after 1 year without penalty

- Only one extension of 3 years is allowed per account

Tips to Maximize Your SCSS Returns

Use these smart strategies to get the most out of your SCSS investment.

Open joint account with spouse. If both you and your spouse are senior citizens, each can have separate SCSS accounts of up to 30 lakh rupees, doubling your investment to 60 lakh rupees.

Time your account opening. Since the interest rate is locked in at the time of opening, try to open the account when SCSS rates are at their peak.

Consider quarterly interest reinvestment. Reinvest your quarterly interest in other instruments like recurring deposits, mutual funds, or PPF for additional growth. Learn more about smart investing in our guide on investment options for beginners in India.

Submit Form 15H. If your total income is below the taxable limit, submit Form 15H at the beginning of each financial year to avoid TDS deduction.

Diversify with other safe instruments. Combine SCSS with PPF, RBI Floating Rate Bonds, fixed deposits, and Pradhan Mantri Vaya Vandana Yojana for a complete retirement portfolio.

Use the right account for interest credit. Link your SCSS account to a high interest savings account from banks like IDFC First, AU Small Finance Bank, or RBL to earn extra interest on credited amounts. Check our complete guide on the best bank for savings account in India for more.

Track quarterly payouts. Maintain a simple record of your quarterly interest credits to manage cash flow effectively. Use one of the best apps for managing personal money in India for hassle free tracking.

Common SCSS Mistakes to Avoid

Avoid these mistakes to make the most of your Senior Citizen Saving Scheme investment.

Investing in lump sum without planning. While SCSS is excellent, putting all your retirement savings in one place is risky. Diversify across instruments.

Forgetting Form 15H. Many senior citizens lose money to unnecessary TDS deduction simply because they forget to submit Form 15H. Submit it every April.

Not nominating beneficiaries. Always update nominee details to avoid legal complications for your family later.

Withdrawing prematurely without need. The 1.5 percent penalty on early withdrawal can wipe out months of returns. Plan your liquidity carefully.

Ignoring tax implications. SCSS interest is taxable as per your slab. Plan your overall income to minimize tax burden.

Missing the extension window. If you want to extend after 5 years, do not miss the 1 year extension window. Mark it on your calendar.

Not splitting across spouses. Many couples miss out on the higher combined limit by not opening separate accounts. Two senior citizens can invest up to 60 lakh rupees combined.

SCSS for Retirement Planning

The Senior Citizen Saving Scheme is one of the strongest pillars of a smart retirement strategy in India. Here is how it fits in.

Use SCSS for:

- Regular quarterly income for daily expenses

- Safe capital protection

- Tax deductions under Section 80C

- Predictable long term cash flow

Pair SCSS with:

- PPF or NPS for long term tax free wealth building

- High yield FDs for additional safe income beyond 30 lakh rupees

- RBI Floating Rate Bonds for higher interest with government backing

- Equity mutual funds (small allocation) for inflation beating growth

- Health insurance for medical emergency coverage

This balanced portfolio gives senior citizens financial security, regular income, and protection against inflation while keeping risk minimal.

How Much Income Can SCSS Generate?

Let us look at realistic income scenarios from SCSS at the current 8.2 percent rate.

For a 30 lakh rupees investment (single account):

- Monthly income: Approximately 20,500 rupees

- Quarterly interest: 61,500 rupees

- Annual interest: 2,46,000 rupees

For a couple investing 60 lakh rupees (30 lakh rupees each):

- Monthly income: Approximately 41,000 rupees

- Quarterly interest: 1,23,000 rupees

- Annual interest: 4,92,000 rupees

For most middle income retirees in India, this can comfortably cover monthly living expenses while also providing protection from market volatility.

Frequently Asked Questions (FAQs)

What is the current interest rate of the Senior Citizen Saving Scheme?

The current Senior Citizen Saving Scheme interest rate is 8.2 percent per annum. This rate is reviewed and updated quarterly by the Government of India. Once you open the account at a given rate, that rate is locked in for the full 5 year tenure.

Who is eligible for the Senior Citizen Saving Scheme?

Indian citizens aged 60 years or above are eligible to open SCSS accounts. Retired civilian employees aged between 55 and 60 years and retired defence personnel aged between 50 and 60 years can also open the account within 1 month of receiving retirement benefits. NRIs and HUFs are not eligible.

What is the minimum and maximum investment amount in SCSS?

The minimum investment in SCSS is 1,000 rupees, and the maximum is 30 lakh rupees per individual across all SCSS accounts combined. Couples can invest up to 60 lakh rupees by maintaining separate accounts.

How is SCSS interest paid?

SCSS interest is calculated and credited every quarter, on the first day of April, July, October, and January each year. The interest is credited directly to the depositor’s linked savings bank account.

Is SCSS interest taxable?

Yes, SCSS interest is fully taxable as per your income tax slab. TDS at 10 percent is deducted if total annual interest exceeds 1 lakh rupees for senior citizens. You can submit Form 15H if your total income is below the taxable limit to avoid TDS deduction.

Can I get tax deduction on SCSS investment?

Yes, the principal amount invested in SCSS qualifies for tax deduction under Section 80C of the Income Tax Act, up to a maximum of 1.5 lakh rupees per year. However, this benefit is only available under the old tax regime, not the new tax regime.

Can I withdraw money from SCSS before maturity?

Yes, premature withdrawal is allowed but with penalties. If withdrawn between 1 and 2 years, 1.5 percent of the deposit is deducted. If withdrawn between 2 and 5 years, 1 percent is deducted. No withdrawal is allowed before 1 year, except in case of the depositor’s death.

Can I extend my SCSS account after maturity?

Yes, you can extend the SCSS account by an additional 3 years after the initial 5 year tenure. The extension request must be made within 1 year of maturity. Only one extension of 3 years is allowed per account.

Where can I open an SCSS account?

You can open an SCSS account at any India Post office or authorized public and private banks including SBI, HDFC Bank, ICICI Bank, Axis Bank, PNB, Bank of Baroda, Canara Bank, Union Bank, Bank of India, and IDBI Bank.

Is SCSS better than bank FD for senior citizens?

For most senior citizens, SCSS is better than bank FDs for the first 30 lakh rupees because it offers a higher interest rate (8.2 percent), government backing, and tax deduction on principal. For amounts above 30 lakh rupees, consider top bank FDs or small finance bank FDs for higher yields.

Final Thoughts

The Senior Citizen Saving Scheme is one of the smartest investment choices for any retiree or senior citizen in India looking for safe, high yielding, and tax efficient returns. With its government backing, attractive 8.2 percent interest rate, quarterly payouts, and Section 80C tax benefits, SCSS continues to be a cornerstone of strong retirement planning.

That said, even the best schemes work better when combined with smart financial planning. Diversify your retirement portfolio across SCSS, high yield FDs, PPF, RBI Floating Rate Bonds, and a small allocation in mutual funds. Always maintain enough liquidity for emergencies, get adequate health insurance, and review your portfolio at least once a year.

If you or your parents have just retired or are planning to retire soon, SCSS deserves a serious look. The peace of mind that comes from a government backed, predictable income stream is invaluable in retirement years.

To take your money journey even further, also explore our complete guides on investment options for beginners in India, best bank for savings account in India, and passive income ideas that actually work to build a complete financial plan.

Are you ready to open your Senior Citizen Saving Scheme account? Visit your nearest post office or authorized bank today, take action, and share your experience in the comments below.

Disclaimer: Interest rates, eligibility criteria, and scheme features mentioned in this article are based on the most recent publicly available data at the time of writing and may change without notice. Always verify the latest details directly from the India Post website, official bank websites, or visit the Reserve Bank of India website before investing. This article is for informational purposes only and does not constitute financial advice. Always consult a SEBI registered financial advisor before making investment decisions.