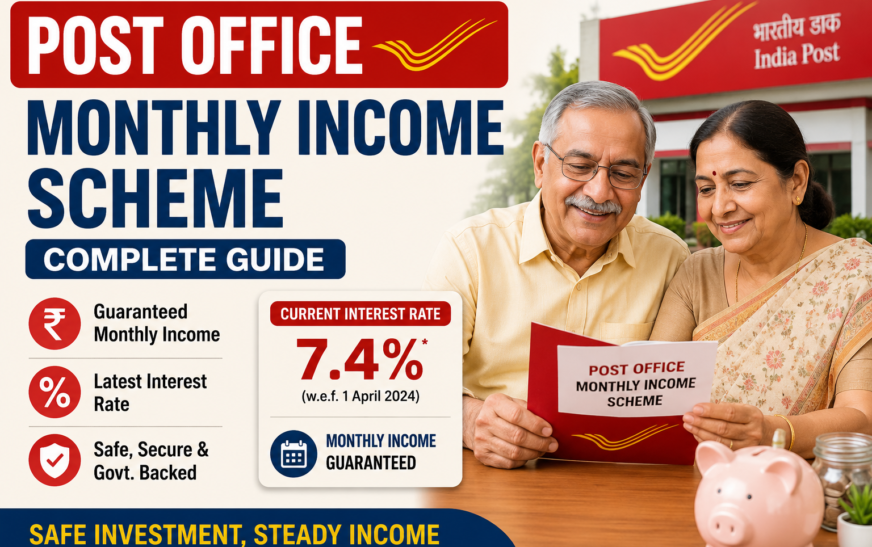

Looking for complete details on the Post Office Monthly Income Scheme (POMIS)? You are in the right place. POMIS is one of India’s most popular government backed savings schemes that offers fixed, guaranteed monthly income to investors who want predictable cash flow without market risk. Whether you are a retiree seeking steady income, a salaried professional looking for an additional income stream, or a conservative investor wanting safe returns, POMIS deserves a serious look.

Backed by the Government of India and operated through 1.5 lakh post offices across the country, POMIS provides assured monthly interest on your lump sum deposit. With no upper insurance limit (unlike bank FDs covered only up to 5 lakh rupees by DICGC), POMIS gives you complete capital protection along with attractive returns paid every single month.

In this complete guide, you will discover everything you need to know about the Post Office Monthly Income Scheme, including the latest interest rate, eligibility, monthly income calculations, tax rules, account opening process, and smart tips to maximize your returns. Let us dive in.

What Is the Post Office Monthly Income Scheme?

The Post Office Monthly Income Scheme (POMIS) is a government backed small savings scheme offered by India Post that provides fixed monthly interest income on a one time lump sum deposit. The scheme is designed for investors who want guaranteed monthly cash flow with complete capital protection.

Key purpose: To generate predictable monthly income for retirees, conservative investors, homemakers, and anyone needing regular cash flow.

Operated by: Department of Posts (India Post), under the Ministry of Communications.

Backed by: Full sovereign guarantee from the Government of India.

POMIS is especially popular among senior citizens, but it is open to all Indian residents aged 10 years and above, making it one of the most accessible income generation schemes in India.

Current Post Office Monthly Income Scheme Interest Rate

The current interest rate on the Post Office Monthly Income Scheme is 7.4 percent per annum, paid monthly.

Key points about the POMIS interest rate:

- The interest rate is 7.4 percent per annum

- Interest is paid monthly to your linked savings account

- The rate is reviewed quarterly by the Government of India

- Once you open the account, the interest rate is locked in for the entire 5 year tenure, even if rates change later

- The current rate of 7.4 percent has been stable since April 2023

This rate is competitive compared to most bank fixed deposit rates and offers the bonus of monthly payouts, making it ideal for income seekers.

If you want to compare POMIS with bank FDs, check our complete guide on banks that give higher interest rate in India for fresh FD options.

Key Features of Post Office Monthly Income Scheme

The Post Office Monthly Income Scheme offers several attractive features.

1. Fixed Monthly Income

POMIS provides guaranteed monthly interest income. The annual interest is divided into 12 equal monthly payouts, giving you a predictable income stream throughout the year.

2. Government Backing

Since POMIS is backed by the Government of India, your capital is fully protected with sovereign guarantee. There is no upper insurance limit, making it safer than bank FDs which are insured only up to 5 lakh rupees per depositor per bank.

3. 5 Year Tenure

The lock in period for POMIS is 5 years. After maturity, you can withdraw the entire principal or reinvest it in a new POMIS account for another 5 years.

4. Affordable Minimum Investment

You can start investing in POMIS with as little as 1,000 rupees, with subsequent deposits in multiples of 1,000.

5. Higher Deposit Limits

POMIS deposit limits were significantly increased in Budget 2023:

- Single account: Up to 9 lakh rupees

- Joint account: Up to 15 lakh rupees (with 2 or 3 adults)

This allows couples and families to earn meaningful monthly income.

6. Multiple Account Holders

You can open multiple POMIS accounts in your name, but the total investment across all accounts cannot exceed the maximum limit (9 lakh for single, 15 lakh for joint).

7. Nomination Facility

You can nominate one or more family members who will receive the account balance in case of your death.

8. Easy Transfer

If you move to a different city, you can transfer your POMIS account to a new post office anywhere in India at no extra cost.

9. Auto Credit Facility

You can choose to receive monthly interest directly into your Post Office Savings Account or your regular bank account through ECS (Electronic Clearing Service).

10. Premature Withdrawal Allowed

While POMIS has a 5 year lock in, premature withdrawal is allowed with applicable penalties after 1 year, giving you emergency liquidity if needed.

How to Calculate POMIS Monthly Income

POMIS interest calculation is simple and straightforward.

Formula:

Monthly Income = (Investment Amount × Annual Interest Rate) ÷ 12

Example calculations at 7.4 percent per annum:

For 1 lakh rupees investment:

- Monthly income: 617 rupees

- Annual income: 7,400 rupees

- Total income over 5 years: 37,000 rupees

- Principal returned at maturity: 1,00,000 rupees

For 5 lakh rupees investment:

- Monthly income: 3,083 rupees

- Annual income: 37,000 rupees

- Total income over 5 years: 1,85,000 rupees

- Principal returned at maturity: 5,00,000 rupees

For 9 lakh rupees investment (maximum single account):

- Monthly income: 5,550 rupees

- Annual income: 66,600 rupees

- Total income over 5 years: 3,33,000 rupees

- Principal returned at maturity: 9,00,000 rupees

For 15 lakh rupees investment (maximum joint account):

- Monthly income: 9,250 rupees

- Annual income: 1,11,000 rupees

- Total income over 5 years: 5,55,000 rupees

- Principal returned at maturity: 15,00,000 rupees

You can use free POMIS calculators on Groww, ClearTax, or Paisabazaar for instant calculations.

Eligibility for Post Office Monthly Income Scheme

The eligibility criteria for POMIS are straightforward.

Eligible to open POMIS account:

- Any individual Indian citizen aged 18 years and above

- Minors above 10 years can open POMIS in their own name (but with parent or guardian as overseer)

- A guardian on behalf of a minor below 10 years or a person of unsound mind

- Up to 3 adults can open a joint POMIS account

Not eligible:

- Non Resident Indians (NRIs)

- Hindu Undivided Families (HUFs)

- Foreign nationals

- Companies, trusts, and other legal entities

Both PAN and Aadhaar are mandatory for opening a POMIS account.

How to Open a Post Office Monthly Income Scheme Account

Opening a POMIS account is simple. Here is the step by step process.

Step 1: Open a Post Office Savings Account First

You need an active Post Office Savings Account to receive the monthly interest payouts. If you do not have one, open it first.

Step 2: Collect the POMIS Application Form

Visit your nearest post office or download the POMIS application form from the India Post website.

Step 3: Fill in the Application Form

Provide the following details:

- Full name as per PAN and Aadhaar

- Date of birth

- Address and contact details

- Deposit amount

- Nominee details

- Joint holder details (if applicable)

- Linked savings account number for interest credit

Step 4: Submit Required Documents

The standard documents needed are:

- Identity proof: Aadhaar card, PAN card, Voter ID, or passport

- Address proof: Aadhaar, utility bill, rental agreement, or passport

- Two passport size photographs

- PAN card (mandatory)

- Aadhaar card (mandatory)

All documents must be self attested.

Step 5: Make the Deposit

Deposit the amount (minimum 1,000 rupees, maximum 9 lakh for single or 15 lakh for joint) by cash, cheque, or demand draft. The deposit date is considered the date the cheque or DD is realized.

Step 6: Receive Confirmation

Once your account is opened, you will receive a certificate or passbook with all your POMIS account details. Keep it safe.

Step 7: First Interest Payout

The first monthly interest is credited to your linked savings account exactly one month after the account opening date. Subsequent payouts continue every month.

Post Office Monthly Income Scheme: Tax Implications

While POMIS offers attractive monthly income, it comes with specific tax implications.

No Section 80C Benefit

Unlike PPF, SSY, NSC, or 5 year TD, POMIS deposits do not qualify for tax deduction under Section 80C of the Income Tax Act.

Fully Taxable Interest

The monthly interest earned on POMIS is fully taxable as per your income tax slab. You must declare it under “Income from Other Sources” in your ITR.

TDS Rules

Currently, TDS is not deducted by the post office on POMIS interest, but you must still declare the income in your tax return.

Section 80TTB for Senior Citizens

If you are a senior citizen, you can claim up to 50,000 rupees deduction on combined interest income from savings accounts, FDs, and recurring deposits under Section 80TTB. However, POMIS interest is generally not covered under 80TTB.

For complete tax planning guidance, visit the Income Tax Department of India website.

POMIS Premature Withdrawal Rules

While POMIS has a 5 year lock in, you can withdraw early with applicable penalties.

Premature withdrawal penalties:

- Before 1 year: Withdrawal not allowed

- Between 1 and 3 years: 2 percent of the deposit amount is deducted as penalty

- Between 3 and 5 years: 1 percent of the deposit amount is deducted as penalty

- At maturity (after 5 years): Full principal is returned with the final interest payout

Death of account holder: The full deposit plus any accrued interest is paid to the nominee or legal heir without any penalty, even before the 5 year lock in is complete.

POMIS vs Other Investment Options

How does POMIS compare with other safe investment options in India? Here is an honest comparison.

POMIS vs Bank Fixed Deposits

POMIS advantages:

- 7.4 percent interest with monthly payout

- Government backed (better than DICGC’s 5 lakh insurance)

- No TDS deduction at source

Bank FD advantages:

- Flexible tenures (7 days to 10 years)

- Easier online management

- Some small finance banks offer 7.5 to 8.5 percent

POMIS vs Senior Citizen Saving Scheme (SCSS)

POMIS advantages:

- Open to all Indians aged 10+

- Lower minimum deposit (1,000 vs typical higher amounts in SCSS)

- Monthly interest payout

SCSS advantages:

- Higher 8.2 percent interest

- Section 80C tax deduction

- Higher 30 lakh rupees deposit limit

Learn more in our complete Senior Citizen Saving Scheme guide.

POMIS vs PPF

POMIS advantages:

- Monthly income payouts

- Shorter 5 year lock in

- No yearly deposit requirement

PPF advantages:

- 7.1 percent fully tax free returns (EEE status)

- Section 80C deduction

- Lock in extension flexibility

POMIS vs Mutual Fund SIPs

POMIS provides guaranteed safety while mutual funds offer higher long term growth potential but with market risk. The smart strategy is to combine both: POMIS for steady income, mutual funds for wealth building.

For more options, check our complete guide on investment options for beginners in India.

POMIS for Senior Citizens and Retirees

POMIS is particularly popular with senior citizens and retirees because it offers:

Guaranteed monthly income. Predictable cash flow for daily expenses, medicines, and lifestyle costs.

No market risk. Unlike mutual funds or stocks, POMIS returns are not affected by market volatility.

Full safety. Government backing makes POMIS one of the safest income options.

Simple management. No complex paperwork or constant monitoring needed.

Lump sum protection. Your principal stays safe and is returned in full at maturity.

For retirees, combining POMIS with SCSS, PPF, and a small allocation in mutual funds creates a balanced retirement portfolio that offers safety, monthly income, and inflation beating growth.

If you are exploring more passive income options, also check our guide on passive income ideas that actually work.

Tips to Maximize Returns From POMIS

Use these smart strategies to get the most out of your Post Office Monthly Income Scheme investment.

Open multiple accounts wisely. Open a single account up to 9 lakh and a joint account up to 15 lakh for combined total exposure of 24 lakh rupees, generating around 14,800 rupees monthly income.

Combine with spouse. A couple can each open single accounts (9 lakh each) and one joint account (15 lakh), totaling 33 lakh rupees and earning roughly 20,350 rupees monthly.

Use ECS auto credit. Set up Electronic Clearing Service to automatically credit your monthly interest to your high interest savings account for additional earnings. Check our guide on the best bank for savings account in India to maximize returns.

Reinvest interest in RD. Transfer your POMIS monthly interest into a Post Office Recurring Deposit (RD) at 6.7 percent for double compounding effect.

Use Auto Sweep for emergencies. Keep emergency funds in a high interest savings account so your POMIS interest can flow into a flexible, accessible source.

Time your account opening. Since the interest rate is locked in at opening, open the account when POMIS rates are at their peak.

Submit Form 15G or 15H. If your total income is below the taxable limit, submit these forms at the bank to avoid TDS on your overall interest income.

Track everything. Use one of the best apps for managing personal money in India to monitor your POMIS payouts alongside other investments.

Common POMIS Mistakes to Avoid

Avoid these traps that can hurt your POMIS returns.

Not nominating beneficiaries. Without nomination, your family may face legal hurdles to access the balance.

Withdrawing too early. The 2 percent penalty between years 1 to 3 can wipe out a year’s worth of interest. Plan your liquidity carefully.

Expecting Section 80C benefit. Many investors are surprised to learn POMIS does not qualify for 80C. Plan your tax saving with other instruments like PPF, ELSS, or SCSS.

Ignoring multiple account rules. Total deposits across all your POMIS accounts cannot exceed the maximum limit. Track this carefully.

Forgetting about taxes. POMIS interest is fully taxable as per your slab. Plan your overall income tax accordingly.

Letting the interest sit idle. If you do not need monthly income for expenses, reinvest the interest in higher yielding schemes like RD, mutual funds, or PPF.

Not splitting between spouse. Many couples miss out on combined limits by opening only one account. Use joint and individual accounts smartly.

How Much Monthly Income Can You Earn From POMIS?

Let us look at realistic monthly income scenarios at the current 7.4 percent rate.

For singles (maximum 9 lakh rupees):

- Monthly income: 5,550 rupees

- Annual income: 66,600 rupees

For couples investing 9 lakh each in individual accounts (total 18 lakh):

- Combined monthly income: 11,100 rupees

- Combined annual income: 1,33,200 rupees

For couples maxing out individual + joint accounts (9 lakh + 9 lakh + 15 lakh = 33 lakh):

- Combined monthly income: 20,350 rupees

- Combined annual income: 2,44,200 rupees

For families investing in multiple ways (different combinations): Income can scale up to 1.5 lakh rupees per month or more by combining POMIS with SCSS, RBI Floating Rate Bonds, and bank FDs.

For most middle income retirees in India, this can comfortably cover monthly living expenses while preserving capital.

Frequently Asked Questions (FAQs)

What is the current Post Office Monthly Income Scheme interest rate?

The current Post Office Monthly Income Scheme interest rate is 7.4 percent per annum, paid monthly. The rate has been stable since April 2023 and is reviewed quarterly by the Government of India. Once you open the account, the rate is locked in for the entire 5 year tenure.

Who can open a Post Office Monthly Income Scheme account?

Any Indian citizen aged 18 and above can open a POMIS account. Minors above 10 years can also open accounts in their own name. Up to 3 adults can hold a joint POMIS account. NRIs, HUFs, and foreign nationals are not eligible.

What is the maximum investment limit in POMIS?

The maximum investment in POMIS is 9 lakh rupees in a single account and 15 lakh rupees in a joint account (with up to 3 adults). The minimum investment is 1,000 rupees.

How much monthly income can I earn from POMIS?

At 7.4 percent per annum, you earn 617 rupees per month per 1 lakh rupees invested. For a 9 lakh single account, the monthly income is 5,550 rupees. For a 15 lakh joint account, it is 9,250 rupees per month.

Does POMIS qualify for Section 80C tax deduction?

No. Investments in the Post Office Monthly Income Scheme do not qualify for Section 80C tax deduction. The interest earned is also fully taxable as per your income tax slab.

Can I prematurely close my POMIS account?

Yes. POMIS allows premature withdrawal with penalties. Withdrawal between 1 to 3 years attracts a 2 percent penalty on the deposit. Between 3 to 5 years, the penalty is 1 percent. Withdrawal is not allowed before 1 year, except in case of the depositor’s death.

Is TDS deducted on POMIS interest?

No, TDS is not deducted on POMIS monthly interest. However, the interest is fully taxable as per your income slab, and you must declare it in your income tax return.

Can I extend my POMIS account after 5 years?

No, POMIS accounts cannot be extended beyond the 5 year tenure. After maturity, you can withdraw the principal or open a fresh POMIS account by depositing the amount again.

Can I open multiple POMIS accounts?

Yes, you can open multiple POMIS accounts. However, the total investment across all your single accounts cannot exceed 9 lakh rupees, and the total across joint accounts cannot exceed 15 lakh rupees.

Is POMIS safer than bank fixed deposits?

POMIS is generally considered safer than bank FDs because it is fully backed by the Government of India with no upper insurance limit. Bank FDs are insured only up to 5 lakh rupees per depositor per bank under DICGC. For large investments, POMIS offers stronger capital protection.

Final Thoughts

The Post Office Monthly Income Scheme is one of the smartest investment options for Indians seeking guaranteed monthly income with full capital protection. With its 7.4 percent interest rate, government backing, easy account opening process, and monthly payouts, POMIS continues to be a favorite among retirees, conservative investors, and anyone looking for predictable cash flow.

That said, POMIS works best when combined with other smart investments. Pair it with the Senior Citizen Saving Scheme for higher returns, PPF for tax free wealth building, and a small allocation in mutual funds for long term growth. This balanced approach gives you safety, monthly income, tax efficiency, and inflation beating growth, all together.

The best part is that POMIS does not require active management. Once you open the account, the monthly interest flows automatically into your bank account for 5 years. You can focus on other financial priorities while POMIS quietly does its work in the background.

To take your money journey even further, explore our complete guides on saving schemes in post office, investment options for beginners in India, and 15 personal finance tips to build a complete financial plan that grows your wealth and protects your future.

Are you ready to open your Post Office Monthly Income Scheme account? Visit your nearest post office today, take action, and share your experience in the comments below.

Disclaimer: Interest rates, eligibility criteria, and scheme features mentioned in this article are based on the most recent publicly available data at the time of writing and may change without notice. All small savings scheme rates are revised quarterly by the Ministry of Finance. Always verify the latest details directly from the India Post website or the RBI website before investing. This article is for informational purposes only and does not constitute financial advice. Always consult a SEBI registered financial advisor before making investment decisions.